Medicare Special Needs Plans in Washington: D-SNP, C-SNP, and I-SNP Explained

Table of Contents

If you've watched TV in the last year, you've almost certainly seen a commercial promising free groceries, dental coverage, or a spending card through Medicare. Some of those ads may be referring to Special Needs Plans, or SNPs, particularly Dual Eligible Special Needs Plans (D-SNPs). But not everyone qualifies for those benefits, and not every advertised Medicare Advantage benefit is tied to an SNP. If you live in Washington and are trying to figure out whether one of these plans is right for you, this breakdown covers all three.

"There are 3 types of Special Needs Plans: Dual Eligible (D-SNPs), Chronic Condition (C-SNPs), and Institutional (I-SNPs). The most common are D-SNPs," says Jim Carroll, a licensed Medicare agent in Titusville, Florida. "These plans are just like Medicare Advantage Plans, but with extra benefits based on the member's specific needs."

Agent comments reflect general Medicare experience and may not describe every plan available in your area. Benefits and eligibility vary by county, carrier, and individual situation.

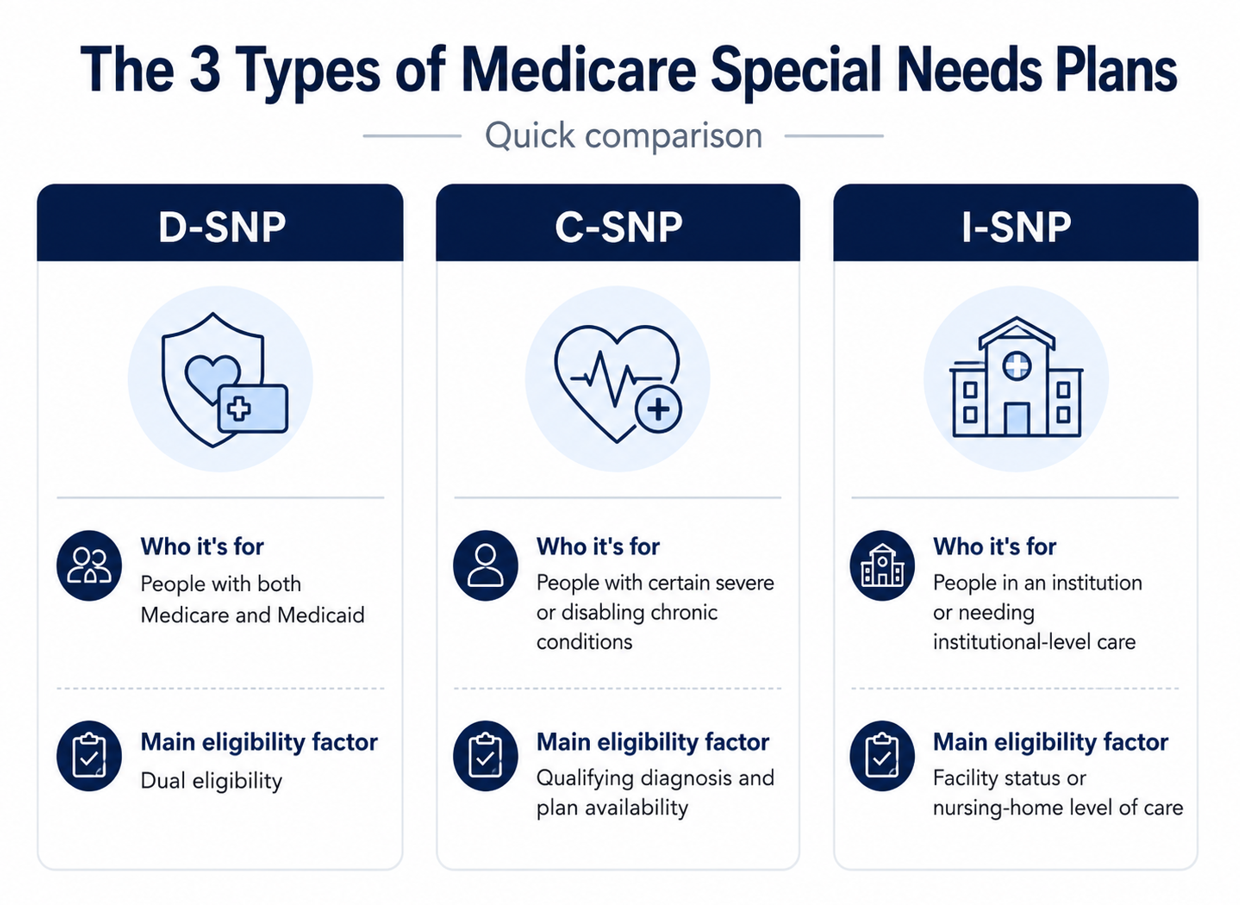

Official Medicare note: Special Needs Plans are Medicare Advantage plans designed for people who have both Medicare and Medicaid, live in or need an institutional level of care, or have certain severe or disabling chronic conditions. Plan availability, benefits, networks, and eligibility vary by county and carrier.

Plan details referenced in this article are based on the 2026 plan year. Benefits, premiums, and availability change annually. Always verify current details on Medicare.gov or with a licensed agent.

SNPs must cover all Medicare Part A and Part B services, but they do so through a Medicare Advantage plan's rules, including provider networks, referral requirements, and prior authorization. Each type also includes additional benefits tailored to its specific group. The catch: you have to qualify. You can't just pick one off a shelf, and the Medicare Advantage plans available to you depend on which carriers serve your county in Washington.

| Plan Type | Who Qualifies | Key Feature |

|---|---|---|

| D-SNP | People with both Medicare and Medicaid | Coordinates benefits to reduce or eliminate out-of-pocket costs; often includes grocery, dental, and transportation extras |

| C-SNP | People with specific severe or chronic conditions (diabetes, heart failure, COPD, etc.) | Tailored provider network, drug formulary, and care management built around the covered condition |

| I-SNP | People who need a nursing-home level of care (in a facility or at home) | Care team coordinates directly with facility staff or in-home providers to manage medications and treatment |

1. D-SNP (Dual Eligible Special Needs Plans)

D-SNPs are by far the most common type, and the ones you see advertised on television. They're built for people who qualify for both Medicare and Medicaid at the same time, a status known as dual eligibility. In Washington, Medicaid eligibility is administered by the state, so specific qualification thresholds and program names may differ from what you see in national ads.

"Oftentimes, I see these D-SNPs with little to no cost as far as co-insurance, copays, and deductibles go," says Brianna Douros, a licensed agent in Virginia Beach, Virginia. "That's gonna depend on your Medicaid level and what you may qualify for."

The key benefits of a D-SNP typically include:

- $0 or very low copays for doctor visits, specialists, and hospital stays

- Prescription drug coverage built into the plan

- Extra benefits like dental, vision, hearing, and transportation to appointments

- A care coordinator who helps manage both your Medicare and Medicaid benefits

- Grocery or healthy food allowances (for qualifying members)

That last bullet is the one driving all those TV commercials. But as Brittany Stickney, an agent in Papillion, Nebraska, points out: "Grocery cards are only available for people who have Medicare and Medicaid. Part B giveback plans are NOT for folks on Medicaid. People on Medicaid have a vastly different experience."

Who Qualifies for a D-SNP in Washington?

You must have both Medicare (Part A and Part B) and some level of Washington Medicaid. Medicaid goes by different names in different states, so check with Washington's Medicaid office if you're unsure whether the program you're enrolled in counts. Your Medicaid category can affect your Medicare cost sharing and which D-SNP options are available to you. The exact benefits you receive depend on Washington Medicaid rules, your eligibility level, and the plan's design.

If you receive both programs, a D-SNP coordinates them so Medicare pays first and Medicaid covers the gaps. This can reduce or eliminate your out-of-pocket costs entirely. Washington residents who think their income might qualify them should explore Medicare Savings Programs as a starting point.

2. C-SNP (Chronic Condition Special Needs Plans)

C-SNPs are designed for people with specific severe or chronic health conditions. Unlike D-SNPs, income and Medicaid status don't matter here. What matters is your diagnosis.

"Here in Arizona and other places too, they have what they call a C-SNP plan," says Steve Brauer, a licensed Medicare agent in Scottsdale, Arizona. "Those plans are designed to be laser-focused for people with chronic illnesses. Most times, their formularies and networks are geared directly toward the chronic condition."

Not every C-SNP is available in every Washington county. Availability depends on which carriers offer chronic condition plans in your specific area, so WA residents should check plan availability by zip code.

Qualifying Chronic Conditions

CMS (the Centers for Medicare & Medicaid Services) maintains a specific list of conditions that qualify someone for a C-SNP. Not every C-SNP covers every condition. The conditions include:

- Diabetes mellitus

- Chronic heart failure

- Cardiovascular disorders

- Chronic lung disorders (COPD and others)

- End-Stage Renal Disease (ESRD) requiring dialysis

- Dementia

- HIV/AIDS

- Certain autoimmune disorders (such as lupus or rheumatoid arthritis)

- Cancer (excluding pre-cancer conditions)

- End-stage liver disease

- Chronic and disabling mental health conditions

- Certain neurologic disorders (such as multiple sclerosis, Parkinson’s, or ALS)

- Stroke

- Severe hematologic disorders

- Chronic alcohol and other substance dependence

CMS recognizes these categories for C-SNP eligibility, but a specific plan may only serve one condition or a limited group of related conditions. A diagnosis alone does not guarantee that a matching C-SNP is available in your county.

The plans that cover conditions like heart disease or diabetes tend to build their entire provider network and drug formulary around managing that condition. For Washington residents managing a chronic illness, this focused approach can be a significant advantage over a standard Medicare Advantage plan.

The Doctor Verification Requirement

One important detail that trips people up: enrolling in a C-SNP isn't the end of the process. Your doctor has to verify your condition.

"When you enroll in a C-SNP plan, you need a doctor, your doctor, to sign off saying you have a chronic special need for this plan," says Voss Speros, a licensed Medicare agent in Mesa, Arizona. "If they don't sign off in the timeframe, then the plan drops. If a plan drops, that creates a new special election period."

This verification is called a Chronic Condition Verification (CCV) form, and you typically have 60 days to get it completed. If you miss that window, you'll be disenrolled from the C-SNP, though you will qualify for a Special Enrollment Period to join another plan. If you need to appeal a plan decision or disenrollment, there is a process for that as well. Washington residents should make sure their doctor's office is aware of this paperwork requirement before they enroll.

3. I-SNP (Institutional Special Needs Plans)

I-SNPs are the least common and least discussed of the three types. They're built for people who live in a nursing home, a skilled nursing facility, or who receive a nursing-home level of care at home.

"Institutional Special Needs Plans are very specific to a nursing home level of care or in a nursing or assisted living setting," says Steven Whetstine, a licensed Medicare agent in Peoria, Arizona.

Who Qualifies for an I-SNP?

I-SNPs are for people who meet one of these criteria:

- Live in a nursing home or skilled nursing facility

- Live in an intermediate care facility

- Live in an assisted living facility that provides certain medical services

- Live at home but require a nursing-home level of care for 90 days or longer

Eligibility usually requires a state-level assessment confirming that you need a nursing-home level of care, even if you live in an assisted living facility or at home.

"Doctors manage care directly where the patient lives," explains Marc Butler, a licensed agent in Deltona, Florida. That hands-on, on-site coordination is the core advantage of an I-SNP: the plan's care team works directly with the facility staff to manage medical decisions, medications, and treatment.

Because I-SNPs serve a smaller population, they're not available everywhere. Washington residents should check whether any I-SNPs are offered in their county, as availability depends heavily on which insurance carriers operate locally.

How SNP Enrollment Works

One of the biggest practical differences between SNPs and regular Medicare Advantage plans is when you can enroll. Standard Medicare Advantage enrollment is tied to specific windows like the Annual Enrollment Period (October 15 to December 7) or the Open Enrollment Period (January 1 to March 31). To enroll in any SNP, you must meet Medicare's basic eligibility requirements first, and then qualify for the specific SNP type.

SNPs are different. If you newly qualify for any type of SNP, you typically have a Special Enrollment Period that lets you join outside of those standard windows. People who qualify for Medicaid, Extra Help, or an SNP may have Special Enrollment Periods outside the standard enrollment windows. The exact timing depends on the reason for eligibility, the type of SNP, and current Medicare rules.

The insurance carriers will require proof of qualification when you enroll. For a D-SNP, that means your Medicaid number. For a C-SNP, it's the CCV form signed by your doctor. For an I-SNP, it's documentation of your institutional or nursing-home level of care.

The TV Commercial Problem

The heavy television advertising around SNPs, particularly D-SNPs, has become one of the most contentious issues in Medicare. Agents across the country say the ads are creating confusion and, in some cases, real harm for beneficiaries who assume advertised benefits are available to everyone.

"There are a few loopholes in Medicare marketing guidelines that allow agents to discuss benefits associated with DSNPs on cold calls," says Gregg Matheny, a licensed agent in Prescott Valley, Arizona. "Unfortunately, I think a commonly used tactic is the bait and switch."

Martin Meyer, an agent in Edwardsville, Illinois, puts it more bluntly: "If you are not on Medicaid, those plans also have extremely high copays and out of pocket limits, which the people calling you usually fail to tell you about."

More broadly, consumers should not assume that a plan advertised with extra benefits will also have low medical cost sharing, especially if they do not qualify for the specific plan type being advertised.

The core issue is that the commercials promote benefits (grocery cards, $0 premiums, spending accounts) that are only available to a narrow group of qualifying beneficiaries. If you don't qualify for Medicaid or don't have a qualifying chronic condition, those benefits don't apply to you. Anyone calling you out of the blue to promise these benefits should be treated with skepticism. Working with a local, independent Medicare agent who can review your actual eligibility is the safest path forward.

Finding the Right Fit in Washington

"Special Needs Plans are a type of Medicare Advantage plan designed for people in specific situations, so the coverage is more tailored to what they actually need," says Justin Kramer, a licensed agent in Humboldt, Iowa. "These plans usually bundle everything together, including drug coverage, and they focus more on coordinated care and extra benefits instead of a one-size-fits-all approach."

If you live in Washington and think you might qualify for a D-SNP, C-SNP, or I-SNP, here's how to work through it:

- Confirm your eligibility. Check whether you have Washington Medicaid (for D-SNPs), whether your diagnosis is on the CMS-approved list (for C-SNPs), or whether your living situation meets the institutional threshold (for I-SNPs).

- Check plan availability in your county. Use the Medicare.gov Plan Finder to see which SNPs are offered in your WA zip code. Not every type is available everywhere.

- Compare benefits, networks, and drug formularies. Two D-SNPs in the same Washington county can have different provider networks, covered medications, and extra benefits. Look at the details, not just the plan name.

- Talk to a licensed agent who knows Washington. For help weighing your overall Medicare plan options, a local agent familiar with Washington's Medicare Advantage eligibility rules and plan landscape can walk you through what's actually available where you live.

Frequently Asked Questions About Medicare Special Needs Plans

Can I get a D-SNP if I only have Medicare, not Medicaid?

Generally no. D-SNPs require both Medicare and Medicaid eligibility. If you only have Medicare, you would not qualify for a D-SNP, though you may be eligible for other types of Medicare Advantage plans.

Are grocery or food allowances available with every Medicare plan?

No. Grocery or healthy food allowances vary by plan and are generally limited to qualifying members of specific plan types, particularly D-SNPs. These benefits are not available to every Medicare beneficiary.

Do all Washington counties have C-SNPs?

No. C-SNP availability depends on the county, the insurance carrier, and the specific condition the plan serves. Not every area in Washington will have a C-SNP option, so WA residents should check plan availability by zip code.

Do I need a doctor to verify my condition for a C-SNP?

Yes. Plans require a Chronic Condition Verification (CCV) form signed by your doctor, typically within 60 days of enrollment. If the form isn't completed in time, you'll be disenrolled from the plan, though you will qualify for a Special Enrollment Period to join another Medicare Advantage plan.

What's the difference between a D-SNP and a regular Medicare Advantage plan?

Both are Medicare Advantage plans, but D-SNPs are specifically designed for people who qualify for both Medicare and Medicaid. D-SNPs include care coordination between Medicare and Medicaid, and they typically offer extra benefits (like grocery allowances, transportation, and expanded dental) that standard Medicare Advantage plans don't provide. You must be dual-eligible to enroll in a D-SNP.

Tammie Rutledge

Licensed Washington Medicare Agent

Contact Tammie through Medicare Agents Hub »

Tammie Rutledge, Licensed Medicare Broker & Certified Senior Advisor

Serving Seniors since 2014. I specialize in Medicare Supplements, Medicare Advantage Plans, Stand Alone Prescription Drug Plans, Medicare and Medicaid Dual Special Needs Plans. Serving Thurston, Mason, Lewis and Pierce Counties in person. Able to serve remotely all of Washington State and other licensed states.