Best Medicare Options for Washington Travelers: Original Medicare vs. Medicare Advantage

Table of Contents

For many Washington retirees, life after 65 isn’t about slowing down, it’s about seeing more of the world. Whether you’re spending part of the year outside WA, taking cross-country road trips, or venturing abroad, your health coverage needs to travel with you. But not all Medicare plans work the same way once you leave Washington.

If you’re a Washington resident who travels often, choosing between Original Medicare and Medicare Advantage (Part C) can make a big difference in how easily you can access care and how much it costs when you do. Let’s break down how each option stacks up for WA travelers who live life on the go.

Key Takeaways for Washington Travelers

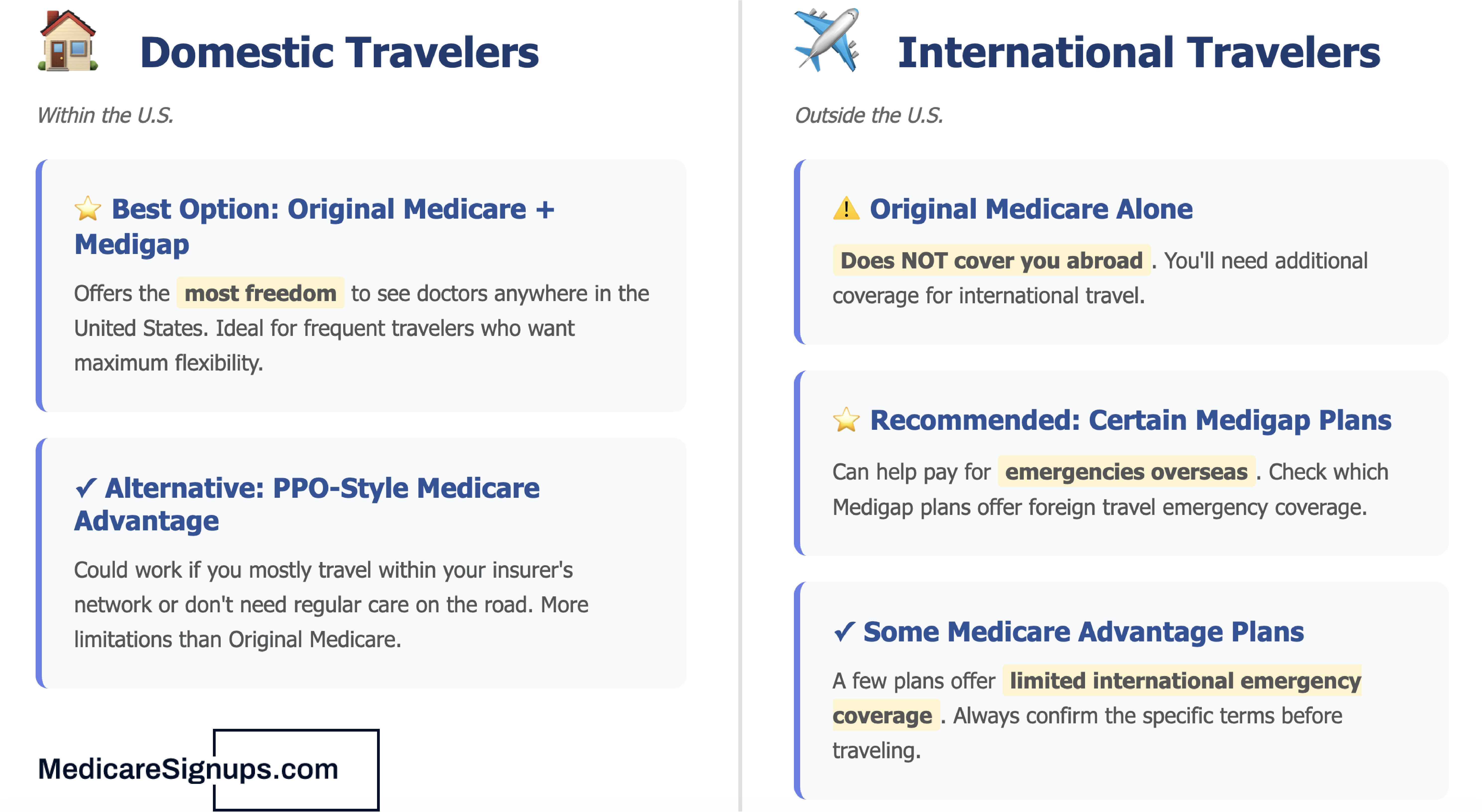

- For U.S. travel: Original Medicare paired with a Medigap plan gives Washington residents the most provider freedom nationwide.

- For international travel: A Medigap plan with foreign travel emergency coverage is essential. Original Medicare alone won’t cover you outside the U.S.

- For Medicare Advantage users: PPO plans travel better than HMOs, but verify the network reaches the places you visit from WA.

- For snowbirds: Confirm any plan covers both Washington and your second home before enrolling.

"There are real options, but the type of plan matters," says Leslie Kaz, a licensed Medicare agent in California. "Original Medicare with a Medigap plan lets you see any doctor or hospital in the U.S. that accepts Medicare, and many Medigap plans like Plan G and Plan N include limited foreign travel emergency coverage. Medicare Advantage PPO plans often let you see providers outside your home area, sometimes nationwide, but your costs may be higher if they’re out-of-network. HMOs usually only cover you in-network, except for emergencies or urgent care while traveling."

How Original Medicare Works When Washington Residents Travel

Original Medicare (Parts A and B) is administered by the federal government, which means your coverage is accepted nationwide by any doctor or hospital that takes Medicare. For Washington travelers, that’s a big plus.

If you’re outside WA and need care, you can typically visit any Medicare-approved provider without needing referrals or worrying about being “out of network.” There’s a freedom here that appeals to snowbirds and cross-country adventurers alike.

Pros for Washington travelers:

-

Nationwide coverage: Nearly any U.S. hospital or doctor who accepts Medicare is an option, whether you’re in Washington or across the country.

-

No provider networks: You don’t have to switch doctors or get special permission to see a new one when traveling outside WA.

-

Ease of emergency care: If you’re injured or fall ill on the road, you can get treated almost anywhere in the U.S.

However, there’s a catch: Original Medicare doesn’t cover care outside the United States in most situations. There are a few narrow exceptions (for example, if you’re traveling between Alaska and another U.S. state through Canada and have an emergency), but these are rare.

If international travel is part of your lifestyle, you’ll likely want a Medigap (Medicare Supplement) plan, specifically one that includes foreign travel emergency coverage. Plans C, D, F, G, M, and N all include up to 80% coverage for foreign travel emergencies during the first 60 days of a trip, after a $250 annual deductible and up to a $50,000 lifetime maximum. Note that Plans C and F are not available to people who became eligible for Medicare on or after January 1, 2020. If you already have one, you can keep it, but newly eligible beneficiaries will need to look at Plan G, N, D, or M for foreign travel emergency coverage.

In short: Original Medicare with a Medigap policy is often the most flexible option for frequent Washington travelers within the U.S., and the best safety net for those who occasionally go abroad.

How Medicare Advantage Plans Handle Travel for Washington Residents

Medicare Advantage (Part C) plans are offered by private insurance companies, and their coverage depends heavily on provider networks. That means your access to care can be more limited when you’re outside your Washington plan’s service area.

Most Medicare Advantage plans available to WA residents are either HMOs (Health Maintenance Organizations) or PPOs (Preferred Provider Organizations). Here’s how they differ for travelers:

-

HMO plans typically require you to use in-network providers for non-emergency care. If you leave Washington, you’ll likely pay the full cost unless it’s an emergency.

-

PPO plans offer more flexibility. You can usually see out-of-network providers outside WA, though you’ll pay more than if you stick with in-network ones.

This is one of the most common surprises agents see. According to Ann Sanfelippo, a licensed Medicare agent in Florida, "if you split time between states, you generally need a plan with nationwide provider access, such as Original Medicare with a Medigap plan. Many Medicare Advantage plans use local or regional networks, so routine care may not be covered when you’re out of state. Some PPO Advantage plans offer limited out-of-network coverage, but it’s often not ideal for long stays."

If you split your time between Washington and another state or frequently move around, this can get tricky. Your Washington ZIP code determines what plans you’re eligible for, and Medicare Advantage plans only have to cover emergency or urgent care outside that area.

It’s also worth understanding the line between emergency and routine care on a Medicare Advantage plan. "Your Medicare Advantage plan covers you for emergencies and urgent care anywhere in the United States, even if the hospital is out-of-network," says James Hale, a licensed Medicare agent in Georgia. "But routine care like regular doctor visits, specialists, and elective procedures is usually only covered inside your plan’s local service area. For frequent or long-term travel, a plan with strong travel benefits, or pairing with a Medigap Plan G, gives you the most freedom."

That said, some insurers are getting more travel-friendly. Certain national PPO networks and Medicare Advantage plans designed for snowbirds allow access to a wider network of providers across multiple states. Others offer telehealth, nationwide urgent care partnerships, or travel coverage programs that make it easier for Washington residents to manage their care while away.

Still, you’ll want to read the fine print carefully, because not every Medicare Advantage plan available in WA offers these features.

Pros for Washington travelers:

-

May include extra benefits like vision, hearing, dental, and fitness programs.

-

Some plans offer emergency coverage abroad.

-

Telehealth access can help you stay connected with Washington providers anywhere.

Cons for Washington travelers:

-

Network restrictions can limit access outside your Washington home area.

-

Out-of-network care may cost significantly more.

-

Plans can vary widely between states, which complicates seasonal moves away from WA.

Domestic Travel vs. International Travel for Washington Medicare Beneficiaries

Your destination matters when it comes to Medicare coverage for Washington residents.

-

Domestic travelers (within the U.S.): Original Medicare plus Medigap offers the most freedom to see doctors anywhere outside Washington. A PPO-style Medicare Advantage plan could work if you mostly travel within your insurer’s network or don’t need regular care on the road.

-

International travelers: Original Medicare alone doesn’t cover you abroad, but certain Medigap plans can help pay for emergencies overseas. A few Medicare Advantage plans offer limited international emergency coverage, but always confirm the terms before leaving WA.

"Original Medicare is a good option for U.S. travel, since it’s accepted nationwide, useful for those with multiple homes or who travel seasonally," says Nicholas Ryckert, a licensed Medicare agent in Florida. "But Original Medicare doesn’t cover everything. Expect significant copays for Part A hospital expenses and about 20% of costs for Part B services with no out-of-pocket limits. And while Medicare works throughout the U.S., it rarely covers care abroad. Consider Medigap or travel insurance to supplement coverage when traveling internationally."

According to Ezel McIntee, a licensed Medicare agent in Oklahoma, "Original Medicare generally does not cover medical care received outside the United States, so you would typically need private travel or international health insurance for coverage while living abroad. Some Medicare Advantage plans may offer limited emergency coverage overseas, but it’s usually restricted and costly."

Don't forget prescriptions. Part D drug plans only cover medications filled at network pharmacies inside the U.S. If you're leaving Washington, check whether your plan has a national pharmacy chain in-network before you go. For international trips, fill prescriptions before departure — Part D won't pay for drugs bought abroad, and Medigap foreign travel emergency benefits don't cover routine medications either.

If you plan to be out of the country for extended periods, you might also want to consider supplemental travel medical insurance (even with Medigap coverage) since Medicare’s foreign travel benefits have dollar and time limits.

Which Medicare Option Is Best for Frequent Washington Travelers?

The right Medicare option for you largely depends on your travel habits and where your adventures take you outside Washington. If you often find yourself exploring different parts of the United States, Original Medicare paired with a Medigap plan tends to offer the most flexibility. This combination allows you to see nearly any provider nationwide without worrying about network restrictions, which makes it ideal for WA residents who spend significant time in multiple states or travel frequently by road or air.

For Washington residents who occasionally travel abroad, a Medigap plan that includes foreign travel emergency coverage provides valuable peace of mind. These plans help cover emergency medical costs outside the U.S., offering an extra layer of protection that Original Medicare alone doesn’t provide.

If you prefer the added benefits that come with Medicare Advantage, such as vision, dental, hearing, and fitness programs, you can still find options that work for Washington travelers. The key is to look for a PPO-style plan with a large or national network, and to confirm that the plan includes travel coverage and telehealth services. These features can make it easier to access care while away from Washington, though you’ll want to double-check the network details for each destination you visit.

For “snowbirds” or Washington residents who split their time between two homes, it’s especially important to verify whether a Medicare Advantage plan covers both areas. If it doesn’t, you may need to switch plans during the Annual Enrollment Period, which runs from October 15 through December 7. Understanding Medicare eligibility requirements and enrollment windows is key to making a smooth transition.

Not sure which travel-friendly plan fits life in Washington?

Talk to a licensed Medicare agent in WA who can compare Medigap and Medicare Advantage options side by side.

Best Options Based on Your Travel Patterns from Washington

When your life takes you beyond Washington, your health coverage needs to keep pace. For Washington residents who want access to any provider across the U.S. or who travel internationally, Medicare with a Medigap policy tends to be the most reliable fit.

Medicare Advantage can still be a great choice for some WA beneficiaries, particularly if you value bundled benefits or primarily stay within one region. Just be sure to verify how your plan handles care away from home before you pack your bags. And if you’re approaching 65 or newly eligible, take the time to compare your options carefully — being aware of common Medicare mistakes can save you from costly surprises when you’re on the road.

Bob Boes

Licensed Washington Medicare Agent

Contact Bob through Medicare Agents Hub »